A couple weeks ago, there was an article in the Gainesville Sun that said the average out-of-pocket expenses for tuition and fees for a bachelor’s degree from the University of Florida was only $10,660. That same day, I happened to be looking at the school’s website and something caught my eye: The school received $724 million in research grants last year. My inner economist quickly realized the incentive problem that leads to poor quality teaching at UF (at least from the perspective of the students I tutor). I did some quick math and confirmed that incentives do in fact matter, even at public universities. Follow the money…

Assuming a four year program, the $10,660 figure translates into $2,665 per year per student (out-of-pocket). The school has 35,043 undergrad students. That means the school collects about $93M per year directly from these students. In other words, they get over 7.5 times more money from research grants than they do from students. (At my Air Force retirement, when asked if I was planning to teach at UF, I joked: “They don’t teach at UF, they write grant proposals.” At the time I didn’t realize how true that statement was.)

Let’s be fair: the school collects more for students than just their out-of-pocket expenses. According to the school’s own numbers, tuition and fees come to $6,380 per year ($22,278 for out-of-state students, who comprise 3% of students). That means the school collects $247M for students (assuming someone else pays the difference). That still makes research grants almost 3 times more than money from students.

So what happens at a school that’s not focused on students? It doesn’t hurt their reputation. UF is ranked #14 for best public colleges by U.S. News & World Report. Part of their formula relies on the student-faculty ratio, which they say is 21:1. (Other sites say the number is 20:1.) A lower number is supposed to imply a student focus because they’re more likely to get more personalized attention from professors. But at a research school, faculty who focus on research may only step into a classroom to lecture to one very large section of students, so the figure could be misleading. A better measure would be actual class sizes. Trying to find the average class size is difficult, but we know what a good standard should be from UF: Their website says “the honors classes are limited to 25 or fewer students.”

What’s the average class size for regular classes at UF? Collegedata.com says “full-time faculty teaching undergraduates” and “regular class size” are not reported. That doesn’t sound like a school that wants to brag about student focus. Collegeconfidential.com has students talking about 300+ and 500+ student classes (a number confirmed anecdotally from students I’ve tutored). Surprisingly, Startclass.com says “Small class sizes (mostly 10-19 students).” UF’s own website says this: “Class size averages depend, of course, on the program, the college and the level of the student. Instructional Faculty & Class Size can be found on the Office of Institutional Research site.”

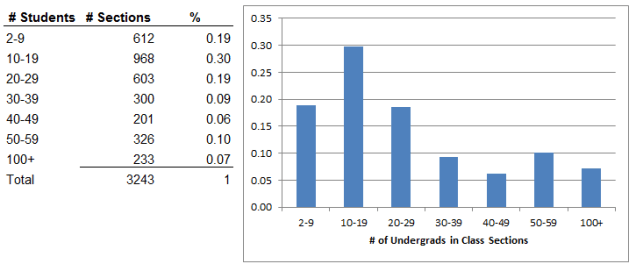

Visiting the link to Office of Institutional Planning and Research shows class sizes from Fall 2012:

That’s where Startclass.com got its number, but while 10-19 is the median size, it’s less than 30% of the total. Realize that classes with 30+ students make up 32.6%, and over a fifth of the classes (23%) have over 40 students. If you remove those honors classes and majors classes, the average class size for freshmen and sophomores will be even worse. Like I said, not student focused.

I don’t mean to imply there aren’t good teachers at UF, or that all professors do not care about their students. I’m just pointing out that it appears quality education (at least as measured by average class size) is not the focus at the institutional level. The money shows why.

You could argue another reason for the lack of student focus is that students pay less than 40% of the cost (and even that is likely paid by parents). That brings up the same third-party payer issues we have in healthcare. That’s a blog post for another time.