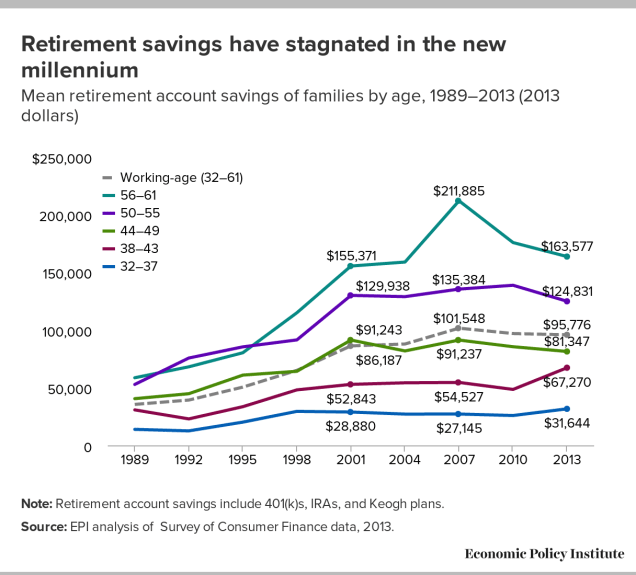

It Already Happened, and the Detractors Are Silent

I touched on Social Security in Chapter 6 of my book, Basic Personal Finance. It was a simple warning to younger generations to not rely on Social Security because the system will not exist much longer in its current state. In 2016, the Board of Trustees of the Social Security trust fund said the annual cost of the program will exceed its income by 2020. Despite repeated warnings by the Trustees over the years, any attempt to modify or privatize the program has been met with vehement opposition, usually from political talking heads with little actual knowledge of economics, finance, investing, or even basic math.

Take LA Times columnist Michael Hiltzik’s 2015 rant as an example. He tried to leverage recent market crashes into emotional appeals to warn against privatization. Anyone can pick and choose specific days for market returns to make things look horrifically bad. You can also pick specific days to turn anyone into a millionaire. Hiltzik’s column ignored long-term trends and the basics of diversification and asset allocation (i.e., moving to safer investments as retirement approaches) and painted Social Security privatization as if it were the end of civilization as we know it.

The funny thing is, privatized Social Security has existed since 1990 for part-time government employees. The 401(a) FICA Alternative Plan allocates 7.5% of these employees’ salaries into pre-tax private retirement plans (similar to a 401(k)). This is done in lieu of Social Security taxes (typically 6.2% from employee and 6.2% from employer). You don’t hear the privatized Social Security detractors complain about this system. Could it be because the perceived benefit of a state government not paying its matching 6.2% Social Security tax somehow outweighs the “dangers” of part-time employees being pushed into a private retirement system instead of Social Security? Imagine the outcry if a private employer tried to weasel out of its matching Social Security contributions.

What if we could all take advantage of a 401(a)-type privatized Social Security system? Part II will look at comparing returns from Social Security and the stock market.